This blog continues on from the events detailed in my previous blog, where a scammer applied for a loan in my wife’s name and then tried to convince her to “repay” the loan from her bank account to one of their choosing.

Their scheme was foiled before it ever really took off, as my wife happened to spot the money, £4,500, in her account before the scammers ever got in contact with her, so by the time they emailed and called she’d already spoken to the loan company’s fraud team.

Their fraud team were very helpful (although completely puzzled as to the point of a scam that involved getting money paid into an account the scammer had no access to). They gave her a fraud reference number, told her to cancel the direct debit that had been set up to repay the loan, said that they would add her to the Cifas voluntary registration scheme (which requires enhanced proof of ID for any credit applications), and that they would contact her bank directly, to reverse the transfer. This all happened on August 11th, and we expected it to be the last we’d hear about it. She’d dodged the scam and done everything right to sort it out. It was all over.

Ha!

In fact, it was the last we heard of it until October 12th, when a letter dropped on our mat, telling my wife that she was in arrears on her loan payments, with an outstanding balance of £7,490.88 (£4,500+interest). This seemed a little unfair, on the grounds that (a) it was the loan company’s own finance team who had said to cancel the direct debit, (b) the money transfer had been reversed, and (c) she’d never taken out a loan in the first place.

The thing was, we realised, that we had no proof of our conversation with the fraud team, no proof that they’d accepted it was fraud, and no proof that they’d advised my wife to cancel the direct debit. If they were going to get heavy, with thing like arrears notices then that raised the possibility that this would end up in court, with us trying to get her to repay money that she’d never asked for and which had already been taken back. Hilarious as that court case would be, it would still be nice to be able to prove our side of the story. For this reason we decided that everything from here on in was going to written.

We emailed the loan company’s customer services team, explaining the whole situation again, and asking three key questions:

- Would they please confirm that my wife didn’t owe them any money and stop sending her arrears notices

- Would they also confirm that they had add my wife to the Cifas scheme

- Would they let her know what details of hers the scammers had used (they wouldn’t do this on her phone call with them in August “for data protection reasons”)

We also said that as the scammers had tried to contact her by phone and by email we’d prefer any response to be via snail mail.

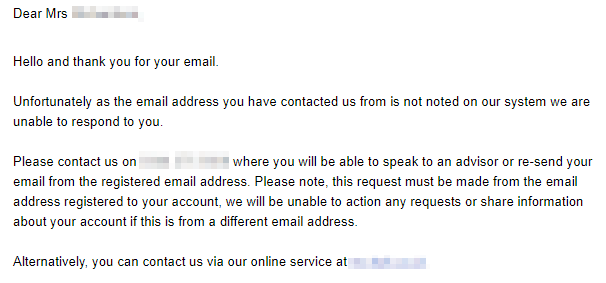

The first thing we were going to learn is that all communications with the loan company have to age for 10 days before anybody sends a response. The second thing was that nobody was spending those 10 days reading what was written. Here’s the first response…

Let’s just take a moment to appreciate the full beauty of that response. In reply to an email saying that scammers applied for a loan in her name, using a false email address, the loan company are saying that they can’t respond, because the email hasn’t come from the email address they have on record.

The one the scammers setup and operate.

The one they wouldn’t tell us, for data protection reasons.

Marvellous.

Still, there was the possibility of contacting them through their secure online portal. That seemed to be an avenue worth exploring.

The initial page of the online portal requires three pieces of information, (i) the loan agreement number, (ii) your postcode, (iii) your date of birth. Once you’ve put those in it gives you a message saying that the information does not match that held on record, and won’t proceed any further. What’s more, as the arrears notice contains both the loan agreement number and our postcode we could be sure that we were in-step with the loan company on those two items, so the erroneous piece of information must be the date of birth used.

The scammers hadn’t even used my wife’s correct date of birth. We emailed back, explaining this, and adding to our list of questions for some sort of explanation as to how even an incorrect DoB hadn’t raised some sort of red flag. Once again, we made it clear that we’d prefer to receive a response by post.

The 10 days to their next reply simply flew by. This one said that as our case sounded like fraud the case details had been passed to the fraud team.

All that happened for the next 3 weeks was that the loan company added another missed payment to my wife’s credit report. We decided to raise a complaint with the loan company and sent them all the details, and our list of questions, again.

This time it only took 4 days for us to get another reply from the customer services team, telling us that, As you have explained in your email that you have had suspicious emails from others in relation to this, we will contact you by letter with any updates.

Woo-hoo! Now we only had to wait 10 days (+2 days to allow for postage) to get an actual physical letter through the post. It acknowledged that we’d raised a complaint, told us it was being investigated, and reminding us that whatever our complaint we must continue to make repayments.

My wife, a defeated woman by this point, left drafting the reply to me.

My wife, perhaps wisely, refused to put her name to this, and we cut it down to a rather boring 2-liner, asking them not to add any more late payments to her credit report.

This time somebody competent seems to have been involved, as inside a week the loan was flagged as “Disputed” on my wife’s credit record, and no further late payment was added.

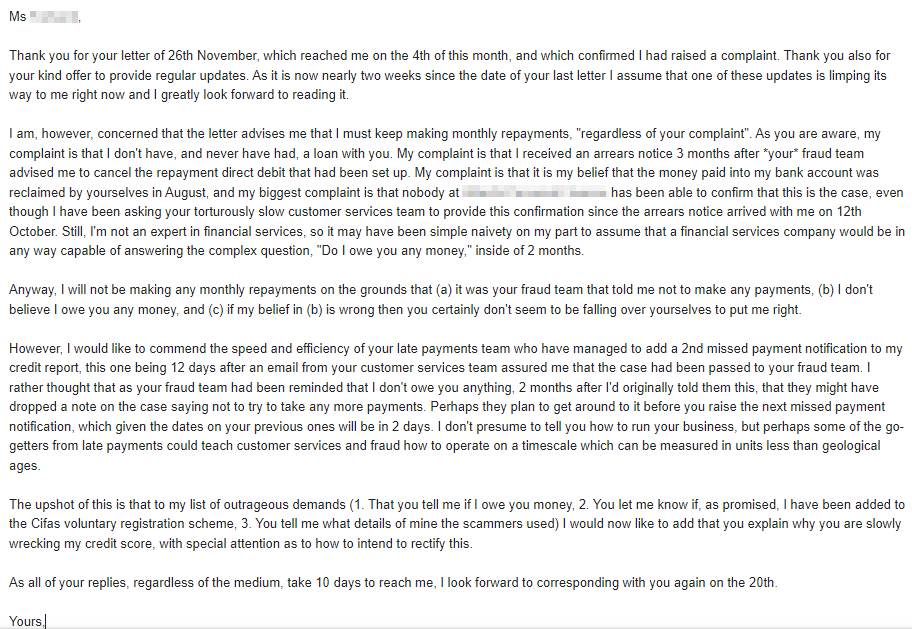

Then, finally, a flurry of activity, and two letters from the loan company in the space of a couple of days. The first was a baffling one, both address to my wife and also referring to her in the third-person. Dear Mrs R, it opens, We’re writing about your request to cancel the agreement with Mrs Lisa R. In case that wasn’t confusing enough, it continues, I’m happy to say that Mrs Lisa R has given their permission to cancel the agreement.

Mrs Lisa R, who has never had an agreement with the loan company, was delighted to hear that Mrs Lisa R has kindly agreed to cancel that agreement, and agrees that the agreement was most disagreeable.

The second letter was more understandable and informed my wife that the investigation had concluded and, more than 2 months after the arrears notice landed, and a full 5 months after her initial contact with the loan company, had decided that fraud had taken place.

There was a certain finality to that letter. A real feeling that things are sorted now, so let’s just draw a line under the whole experience.

My wife, who had contacted the loan company at 9am the day after the money appeared in her account still has 2 missed payments on her credit record for a loan she never took out.

The loan company have not answered a single one of the questions she raised.

If they don’t soon then this blog will be edited, to name them.

[…] The story continues here […]

LikeLike